“Hindsight is notably cleverer than foresight.”

Chester W. Nimitz

Few years in recent history have received the unanimous ire and contempt bestowed upon 2020. No tears were shed as the calendar flipped on this hellacious year. And while the virus pays no regard to the earth’s rotations around the sun, the new year begins with the optimism of initial vaccinations.

At this point, most financial commentaries would segue into bold forecasts for the year to come. We’ve never been fans of predictions, particularly about the future, and are thus taking the unpopular decision to look back at the year that most of us would rather forget.

We do so not as a form of masochism but with our investors in mind. The events of 2020 provided a litmus test for one’s business and investment strategy, exposing and exacerbating both the strengths and weaknesses.

Thus, we proceed in the spirit of transparency, to offer our clients a greater understanding of our strategy, what transpired over the past twelve months, and where that leaves us now.

The calm before the storm.

Despite news of a novel coronavirus surfacing in China, the year began with equity markets reaching new highs and credit spreads locked in a range of a few basis points. During these initial weeks, we focused on security selection and executing our trading strategies to generate excess returns.

In mid-February, we felt that segments of the credit market, in particular derivatives, were underpricing the inherent risks. Accordingly, we built a short position in the CDX derivative index as a partial hedge for our exposure. These hedges blunted the pain from the initial sell-off but were less effective once the problem became one of liquidity.

The eye of the storm.

The severe scarcity of cash had market participants selling what they could to fund their obligations. The securities of choice were high-quality, short-dated corporate bonds, exactly where the fund was concentrated. This dash for cash led to a violent and dramatic widening of credit spreads, with three-quarters of the 2008 move occurring in a matter of a few weeks.

The mark-to-market losses were far greater than we could have imagined for this strategy over such a short period. While the drawdown was painful there were some silver linings during those dark days:

- The portfolio yield rose to exceed 20%.

- Given the high quality (98% investment-grade) and short maturity profile (average < 2y), the risk of permanent loss of capital due to default remained minimal.

- Our leverage limit ensured sufficient excess margin.

- We incurred minimal redemptions and raised assets during this period, by providing our investors with clear, transparent, and informative communications.

The combination of the above factors meant the Fund wasn’t forced to sell securities at the lows and lock-in losses. Furthermore, the nature of the strategy and resilience of investment-grade bonds gave us confidence that we would recoup the losses. We were nonetheless very pleased when the cavalry turned up with unprecedented stimulus packages.

The clouds begin to part.

The central banks were quick to flood the market with liquidity, while government programs reduced the risk of widespread insolvencies. These measures directly addressed the factors driving spreads wider. Furthermore, the Federal Reserve and Bank of Canada added more support when they introduced corporate bond purchasing programs.

Given the scale of the stimulus, we elected to unwind our derivative hedges and increase the Fund’s overall credit exposure. Our initial focus was on taking advantage of the attractive valuations in ‘no brainer’ sectors such as grocers, utilities, banks, and telcos. But as markets stabilized and liquidity returned, we re-engaged our trading strategies and focused on issuer analysis and credit selection.

The path to recovery.

Through our research and analysis, we segmented the universe of companies into four categories:

- Resilient Businesses – businesses unimpacted by or benefitting from the pandemic (i.e. grocers, telcos)

- Goldilocks Companies – relatively resistant and resilient businesses with attractive valuations (i.e. asset managers, public pensions, grocery-anchored REITs)

- Recovery Plays – issuers that are dependent on economic recovery (i.e. autos, construction) or support from policymakers (i.e. financials, banks)

- Directly Affected Businesses – distressed companies with unattractive business profiles (i.e. tourism, hospitality, covered malls)

During the first phase of the market recovery, we concentrated on resilient and goldilocks credits. As valuations became less attractive in the unimpacted issuers, we rotated to more goldilocks names and added some recovery plays. Once news of the vaccines surfaced, we increased exposure to issuers benefitting from the recovery and selectively added some high-quality directly affected businesses.

Bringing it home.

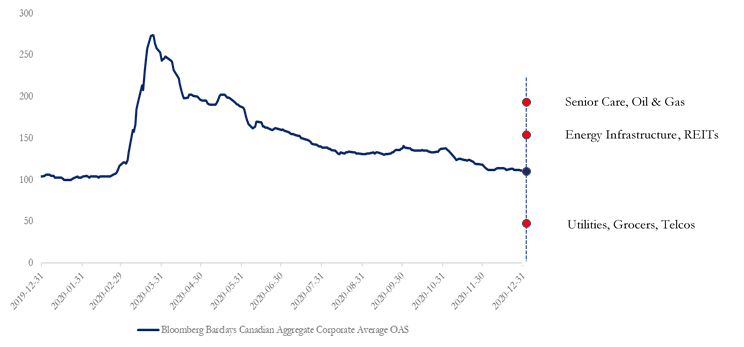

Since the ‘wides’ of March, credit indices have almost recovered to pre-pandemic levels. But much like equity markets, there is significant dispersion amongst issuers and sectors.

Generic Investment-Grade Credit Spreads:

- Canadian spreads widened 7 bps in 2020 to finish at 111 bps

- US spreads widened 3 bps in 2020 finishing at 96 bps

While credit didn’t fully rebound from the March sell-off, the Fund managed to recover from the ugliness of the first quarter to finish the year +4.44%. The resiliency of the strategy meant not only were we able to withstand the storm but also increase exposures into the rally.

In retrospect, we wish we had been a bit more aggressive and had more exposure to businesses hard-hit by the pandemic. But hindsight is 2020 (bad pun intended), and speculating on the timing of a vaccine felt imprudent. Thus, with the information available at the time, and capital preservation in mind, a medium level of risk seemed appropriate as we navigated this most unpredictable of years.

| 1M | 3M | 6M | 2020 | 1Y | 3Y | 5Y | SI | |

| X Class | 1.26% | 3.89% | 10.44% | 4.44% | 4.44% | 4.69% | 8.91% | 10.19% |

| F Class | 1.14% | 3.52% | 9.93% | 3.67% | 3.67% | 3.90% | NA | NA |

As of December 31st, 2020

The Algonquin Debt Strategies Fund LP was launched on February 2, 2015. Returns are shown on ‘Series 1 X Founder’s Class’ since inception and for ‘Series 1 F Class’ since May 1st, 2016 and are based on NAVs in Canadian dollars as calculated by SGGG Fund Services Inc. net of all fees and expenses. For periods greater than one year, returns are annualized.

While certainly not deserving of a parade, when we think back to the pit of despair that was March, talk of producing a positive outcome by year-end seemed to be the ramblings of a mad man.

Looking Ahead.

The natural question on everyone’s mind is, “where do we go from here?”

On the surface, credit spreads appear to be back to where they started in 2020. While this is true of the index, the dispersion across issuers and sectors is remarkably high.

Not all credits are created equal.

The spreads of resilient sectors are well below the average and at levels not seen in over a decade. Meanwhile, the recovery names and directly affected businesses are trading significantly higher than a year ago. Through careful analysis and issuer selection, we look to extract value and capture attractive spread performance as economic activity improves.

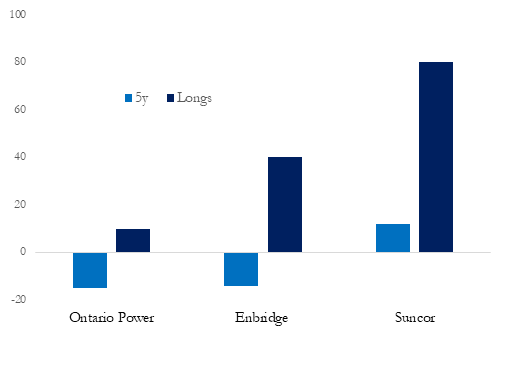

The trouble with the curve.

The other interesting opportunity for us lies along the curve.

YoY Credit Spread Changes

Given concerns over inflation and long-term interest rates rising, investors are reluctant to buy longer-maturity bonds. As a result, credit spreads in maturities greater than 7 years are much wider than they were before the pandemic, even for the resilient issuers.

Since the Fund hedges interest rate risk and isolates the credit exposure, we are uniquely positioned to take advantage of this very attractive opportunity.

Volatility knocks.

With politicians and central bankers leaning towards more stimulus and multiple vaccines receiving approval, we expect a strong but uneven recovery ahead. While the expectation is for a rebound in growth and earnings, the market rarely travels in a straight line, and we still have the virus and stiffer lockdowns to contend with.

The increased volatility positions our active trading strategies to generate excess returns. As the economic data evolves, new issues come to market, and yield curves gyrate, we look to capitalize on the pockets of opportunities created by the movements.

Our other preoccupation.

Outside of obsessively worrying about the Fund, our other preoccupation has been the social impact of this period. The pandemic has disproportionately affected certain segments of society and exacerbated many social and economic problems.

One such sad consequence has been the rise in domestic violence. At the same time, the organizations supporting the victims and survivors of abuse are facing funding uncertainties. To help bridge the gap, we initiated Algonquin’s giving program with significant donations to the Assaulted Women’s Helpline & Senior Support Line, and two local shelters, Nellie’s and the Redwood.